Speech by Bank of Greece Deputy Governor John (Iannis) Mourmouras at the “Asset and Risk Management Seminar for Public Sector Investors” in Singapore: “Global risks in an era of negative interest rates”

29/03/2016 - Speeches

Speech by

Professor John (Iannis) Mourmouras

Deputy Governor, Bank of Greece

Former Deputy Finance Minister

“Global risks in an era of negative interest rates” *

Singapore, 29 March 2016

Ladies and Gentlemen,

It is a great pleasure for me to be here in Singapore and I would like to thank the Lee Kuan Yew School of Public Policy of the National University of Singapore and OMFIF for inviting me to speak to you today.

My speech will be structured in two sections. The first section looks into today’s negative interest rate world, dissecting the factors that have brought us here and also exploring the theory behind, and the limits of, a negative interest rate policy and its potential hazards. Section 2 analyses other downside risks for global markets, placing particular emphasis on China and its huge private debt, on the sharp fall in oil prices, and on Brexit.

1. On negative rates

1.1 Living in a negative interest rate environment

After nine years of low interest rates and large-scale market interventions, the consensus is that this unconventional monetary policy is not temporary, while in most advanced economies the prospect for normalisation seems rather remote. Indeed, most of continental Europe (the euro area, Denmark, Sweden and Switzerland) and, as of last January, also Japan have moved towards a much more accommodative monetary policy by introducing negative policy interest rates, and/or negative central bank deposit rates. Together with forward guidance and quantitative easing, such measures have created an unprecedented situation, in which nominal interest rates are negative in a number of European countries across a range of maturities in the benchmark yield curve, from overnight to even five- or ten-year maturities! Indeed, 88 of the 346 securities in the Bloomberg Eurozone Sovereign Bond Index have negative yields, thus nearly $2 trillion of debt issued by European governments is currently trading at negative yields. Illustrative examples are those of Switzerland and Germany, in which 18 out of 19 bond issues and 14 out of 18 bond issues respectively are priced with negative yields. As a result, almost one quarter of the world’s GDP is produced in countries with negative interest rates.

A chronicle

Sweden’s Riksbank was the first central bank to experiment with negative interest rate policy, or NIRP as it has been commonly known, briefly moving the rate it pays on commercial bank deposits to -0.25% in 2009. In February 2016, it brought its benchmark interest rate even further into negative territory, to a record low of -0.5% from -0.35%, not having met its 2% inflation target for four years. The second central bank to have taken similar actions by setting its deposit rate below zero was the Danmarks Nationalbank (DNB), which in early July 2012, cut its certificate of deposit rate from zero to -0.20%, while in early 2015, it pushed this rate to as low as -0.75%.

The Swiss National Bank (SNB) announced the introduction of negative interest rates (-0.25%) on sight deposit account balances in December 2014 (effective 22 January 2015). In mid-January, with pressure on the Swiss franc unabated, the SNB discontinued the minimum exchange rate and lowered the interest rate on sight deposit accounts further to -0.75%.

Last but not least, in January 2016, the Bank of Japan (BoJ), which has seen the effects of its last stimulus package dissipate as a result of tax increases and slowing demand from China, cut the rate it offers on new deposits to -0.1%, from 0.1%, adopting a three-tier system for interest rates on excess reserves. Under the planned three-tier scheme, the average outstanding balances of excess reserves that each financial institution held in 2015 will still have the current interest rate of 0.1%. This could be deemed the BoJ’s way of showing its consideration for financial institutions’ cooperation towards monetary base expansion via Quantitative and Qualitative Monetary Easing (QQE). A zero interest rate will be applied to the statutory required reserves plus the reserve balance corresponding to the credit provided through the BoJ’s various loan support programs. In addition, as the excess reserves increase alongside the BoJ’s continued buying operations of Japanese Government Bonds (JGB), a certain ratio of these new reserves (“macro add-on”) will be subject to the zero rate. Thus, the penalty rate of -0.1% will only be applied to a fraction of the excess reserves, as the BoJ is concerned about minimising the damage to banks’ earnings.

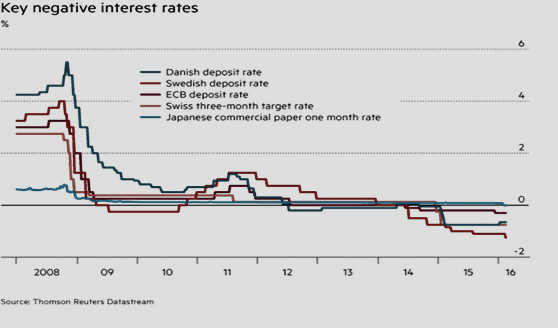

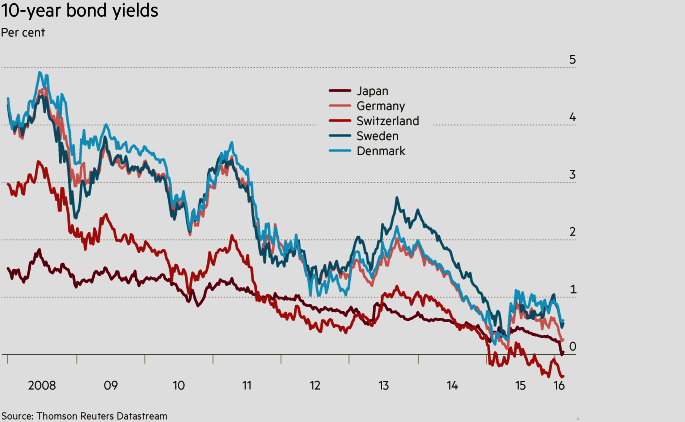

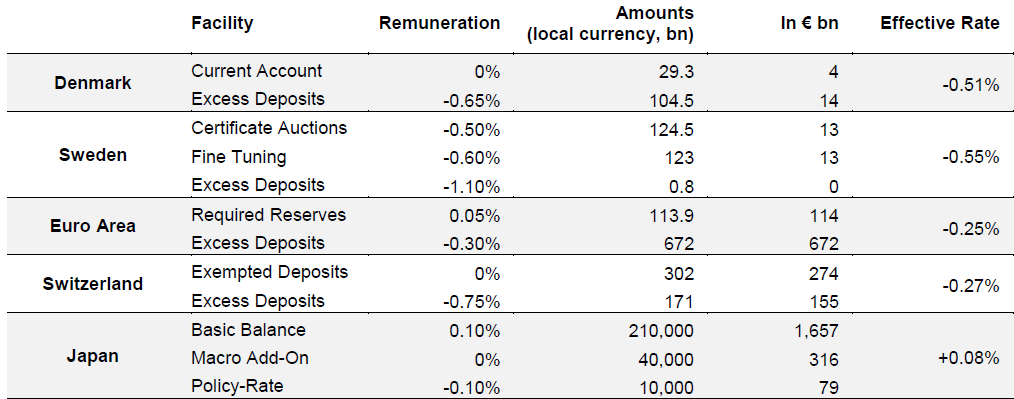

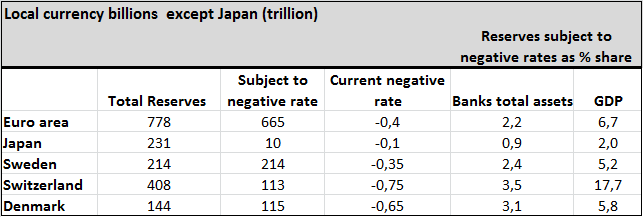

The following figures (Figure 1, Figure 2) clearly show the current key negative rates for the central banks I just mentioned and the very low levels of the 10-year government bond yields of Germany, Denmark, Switzerland, Sweden and Japan. Moreover, Japan is the second country to sell 10-year bonds at a negative yield, after Switzerland last April. Tables 1-3 also provide detailed information about the impact of negative rate regimes on liquidity and retail rates.

Figure 1. Current key negative interest rates

Figure 2. 10-year government bond yields

Table 1. Policy rates and attitudes to draining liquidity at central banks with negative interest rate policies

Table 2. Central banks’ negative interest rate regimes

Table 3. Pass-through of policy rates to the retail level (new business)

.png)

1.2 The ECB’s recent policy stance

Turning to the euro area’s case, let me quickly remind you of the ECB’s monetary policy stance over the last nine years as a response to the worst financial crisis since the Great Depression, leading to negative interest rates and entering practically unchartered territory (Table 4).

Table 4. ECB’s non-standard measures

|

Year

|

Non-standard measures

|

|

Oct-Dec 2008

|

ECB cuts the base interest rate from 4.25% to 2.50%, provides US dollar liquidity through foreign exchange swaps, expands the list of assets eligible as collateral in Eurosystem funding operations, introduces the 6-month longer-term refinancing operations (LTROs) and decides the main refinancing operations to be carried out through a fixed-rate tender procedure with full allotment.

|

|

2009

|

ECB cuts the base interest rate from 2.50% to 1.00%, and introduces the first Covered Bond Purchase Programme (CBPP1).

|

|

2010

|

ECB activates the Securities Markets Programme (SMP).

|

|

2011

|

The ECB launches the second Covered Bond Purchase Programme (CBPP2) and introduces the 3-year LTROs.

|

|

2012

|

The ECB announces the Outright Monetary Transactions (OMTs).

|

|

2013

|

The ECB cuts the base interest rate to 0.25% and introduces forward guidance.

|

|

2014

|

The ECB cuts the base interest rate to 0.05% and the deposit facility rate to -0.20%, bringing it for the first time in negative territory and introduces the Targeted Longer-Term Refinancing Operations (TLTRO) with a 4-year maturity.

|

|

2015

|

ECB introduces the expanded Asset Purchase Programme (APP) and cuts the deposit facility rate to -0.30%.

|

|

2016

|

ECB accelerates the expanded Asset Purchase Programme (APP) and cuts the Main Refinancing Operations (MRO) rate to 0.00% and the deposit facility rate to -0.40%.

|

1.3 Some theory behind negative policy interest rates

In theory, the transmission of negative policy interest rates to economic activity should be close, but not similar, to a standard rate cut that leaves policy rates positive. Let me explain. One thing is a drop in interest rates from 2% to 1%, from 1% to zero, but another thing is a drop from zero to -0.5% to -1% and so on.

Economists used to think that policy interest rates could not fall below zero. They talked about nominal interest rates having a “zero lower bound” (ZLB), but we know now that the lower bound to interest rates is not exactly zero, but below zero! I focus here on the transmission mechanism and on cash hoarding.

A. Targeting interest rates to negative territory will reduce the costs to borrow for companies and households, driving demand for loans and incentivizing investment and consumer spending affecting the outlook for the economy, influencing confidence. These changes will in turn affect the investment and saving decisions of businesses and households, which should raise demand for domestically produced goods and services. By discouraging capital inflows, there will be downward pressure on the exchange rate, which should support external demand. Here are the transmission channels related to negative interest rates.

Table 5. Negative interest rate policy (NIRP): transmission channels

|

Transmission Channels

|

Outcome

|

|

Credit Channel

|

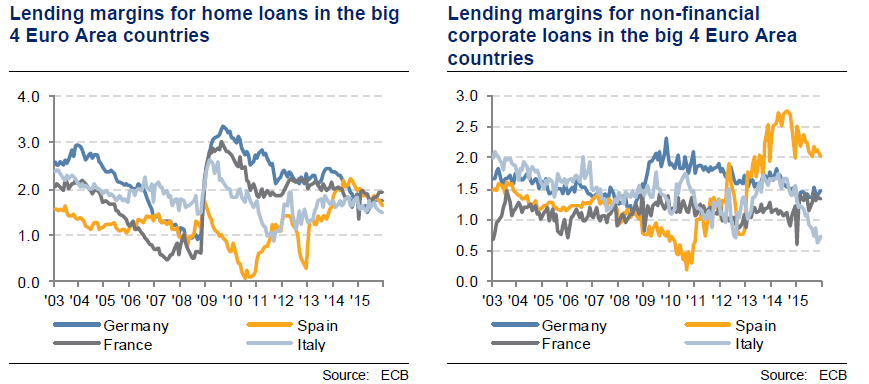

Reduced fragmentation in euro area lending margins for home loans and non-financial corporate loans (see Figure 3).

|

|

Asset Valuation Channel

|

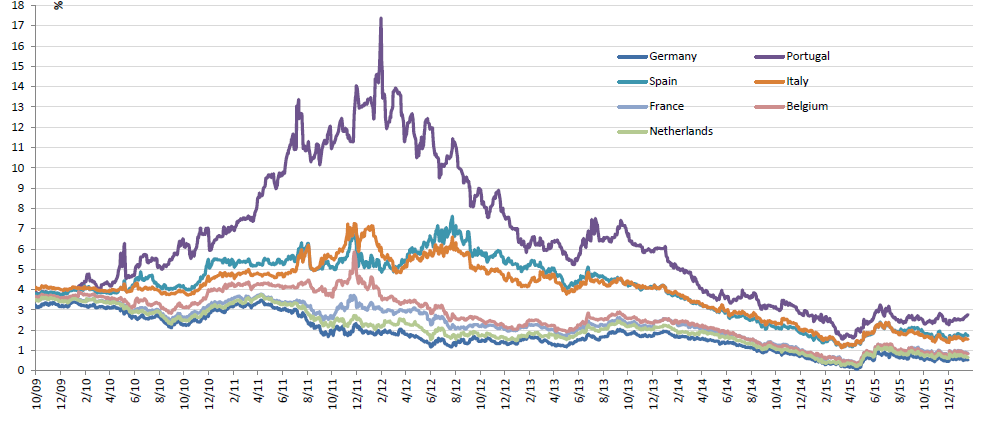

Reduced fragmentation as negative interest rates have pushed down yields in core euro area countries and, indirectly, in other European countries, reducing their spreads (see Figure 4).

|

|

Expectations channel

|

The latest inflation figure for the euro area was lower than expected at -0.2% in February, reinforcing expectations for further rate cuts from the ECB, as in the end decided in March.

|

|

Exchange Rate Channel

|

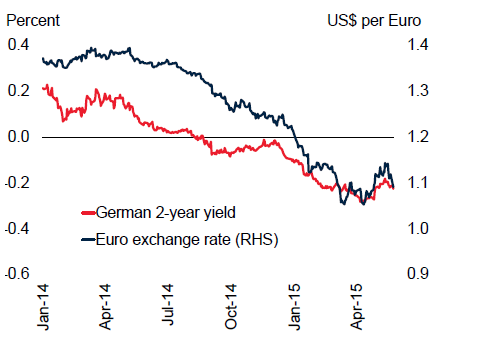

Declines in nominal interest rates from any level can trigger a depreciation of the currency (see Figure 5). From June 2014, when ECB imposed a negative deposit facility rate, the euro has depreciated by more than 19% against the US dollar, while, according to the OECD, the depreciation should contribute to euro area growth by around half a percentage point.

|

And here is the evidence.

Figure 3. Euro area lending margins for home loans and non-financial corporate loans

Figure 4. 10-year bond yields in selected euro area countries

Figure 5. Euro/dollar exchange rate and government bond yields

B.

B. Holding cash is costly for people as it involves storage, insurance, handling and transportation fees (what macroeconomists call ‘shoe-leather’ costs). In fact, the cost of holding cash is what defines the effective lower bound on policy interest rates (i.e. the real constraint on the ability of central banks to set negative interest rates). Central banks can, in effect, safely reduce their policy rates in the amount of storage and insurance costs of money holdings without triggering widespread switching to cash in the economy. But once policy rates fall too far into the negative zone, i.e. below the costs of holding cash, people will start to hoard money instead of holding the negative yielding deposits. At this point, cash will be held by people merely as a store of value, indistinguishable from bonds, banks will be left with less deposits and the economy with fewer loans.

1.4 Potential risks from negative rates policy

There are, however, a number of concerns associated with the use of negative interest rates, each of which is considered in turn.

I. Erosion of bank profitability: As negative deposit rates impose a cost on banks with excess reserves, there is a higher probability that the banks’ net interest margins (the gap between commercial banks’ lending and deposit rates) will shrink, since banks may be unwilling to pass negative deposit rates onto their customers to avoid an erosion of their customer base and subsequent reduced profitability. The extent of the decline in profitability will depend on the degree to which banks’ funding costs also fall. The central bank could reduce concerns about bank profitability by raising the threshold at which the negative central bank deposit rate applies, as the Bank of Japan recently introduced a three-tier system, a different way from the ECB’s negative interest rate policy. Doing so, however, it could reduce the transmission of negative deposit rates to market rates, namely the power of negative interest rate policy transmission through the credit and portfolio rebalancing channel. Moreover, compressed long-term interest rates also reduce profit margins on the standard banking maturity transformation of short-term borrowing and lending at a somewhat longer term. So far, lenders have been reluctant to pass on the costs of negative rates to customers and have taken almost all of the burden. But, as recent research by the BIS shows, the impact on profitability becomes more drastic over time, as short-term benefits such as lower rates of loan defaults diminish.

II. Negative effects on financial markets: Money market funds make conservative investments in cash-equivalent assets, such as highly-rated short-term corporate or government debt, to provide liquidity to investors and help them preserve capital by paying a modest positive return. While these funds aim to avoid reductions in net asset values, this objective may not be attainable if rates in the market are negative for a considerable period of time, prompting large outflows and closures and reducing liquidity in a key segment of the financial system. For insurance and pension funds, a low-for-long interest rate environment poses challenges, which may even be exacerbated if rates enter into negative territory. They may find themselves unable to meet fixed long-term obligations. Life insurance companies will also be less able to meet guaranteed returns.

III. Excessive risk-taking: Increased financial stability risks, stemming from search for yield and higher leverage. Keeping interest rates at negative levels for a long time increases borrowing attractiveness in key sectors of the economy and the risk of bubbles. This can not only lead to an inefficient allocation of capital, but leave certain investors with more risk than they appreciate, as investors in search of higher yields necessarily turn to excessive risky assets.

IV. Disincentive for government debt reduction: With interest rates at negative levels, governments are under no pressure to reduce their debt. Negative rates actually encourage them to borrow more. And if government borrowing becomes a sort of free lunch, there is a clear disincentive for fiscal discipline. Ultra-low interest rates flatter the debt service ratio, painting a misleading picture of debt sustainability. For instance, persistent negative rates may potentially act as an "anaesthetic" to governments of eurozone countries, especially in the europeriphery, meaning that they will proceed only slowly with fiscal and structural reforms, given the fiscal space that they gain from lower debt servicing costs..

V. Operational risks: The issuance of interest-bearing securities at negative yields may face design challenges. Areas that are commonly mentioned as sources of concern are interest-bearing securities, particularly floating-rate notes (renegotiating, collecting interest, use as collateral) in the context of negative interest rates. More generally, if negative rates were to prevail for long, they may entail the need to redesign debt securities, certain operations of financial institutions, the recalculation of payment of interest among financial agents, and other operational innovations, the costs of which may offset negative rate benefits. For instance, most option-pricing models either do not work or do not work well with negative interest rates, particularly entailing risks for the compatibility of trading systems and other market infrastructure.

In brief, persistent negative rates may change expectations and create distortions (for instance, in terms of saving habits and, in that sense, they may be a topic for behavioural economists to look at). It is still unknown what their long-term effects will be (e.g. on the erosion of bank profitability). In contrast, QE has been tested successfully in the US and the UK and I would also like to remind you that monetary policy– conventional or unconventional – entails considerable time lags. It takes time to see the results at full length. However, there is definitely something positive about negative interest rates: it is a strong reminder that the time has come for other policy tools, including fiscal and structural ones.

2. Other global risks

2.1 China

Let me now turn to other global risks, starting with a country in this region of the world: China. Three are the major risks concerning China, stemming from: a) its lower growth prospects, b) significant capital outflows, and c) rising private debt. China is beginning to rebalance and consolidate its economy. Services now account for 51% of GDP and consumption’s GDP share is rising, while the current account surplus dropped to 2.7% from 10% in 2007. Even if you accept the lower expected growth rate for China around 6% in 2016, trade flows to the rest of the world are not significant and this is in contrast with financial flows.

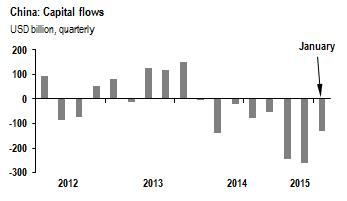

Figure 6. Chinese capital outflows

Only recently I had been invited to give a personal verdict at an event in London and rank the above three downside risks facing China, namely lower growth prospects, capital outflows (almost US$160 billion exited the economy in December 2015, reaching an aggregate amount of almost US$1 trillion in 2015, see above Figure 6) and private debt (which accounts for about 210% of China’s GDP). I gave the following ranking from bottom to top. At the bottom, I would place capital outflows, since the instrument of capital controls is always available and these days indeed with the blessing of the IMF. I would then place in second position the rise in private debt, since only less than 1% of it is held by foreigners, and it can be easily turned into public debt, if it comes to the worst, and I mean by that, all these state-owned zombie companies which may lose their state guarantees, but whose debt may well be acquired by the government, thus increasing China’s public debt ratio, which is now low at 60% of its GDP. Leaving at the top, as the biggest risk, the rebalancing of the economy which, however, will take years and, in my view, markets will have to learn to live with this.

2.2 Oil prices

Since June 2014, oil prices have declined by more than 70%, after having stabilised above US$100 per barrel for four years and, more generally, after rising almost continuously since early 2000. By January 2016, oil prices traded around US$30 per barrel, a level not seen in the past 12 years (see Figure 7 below).

In the context of weak global growth and zero or negative rate monetary policies, lower oil prices are both a fiscal and monetary policy challenge for major economies. While the positive impact on oil importer countries, and especially households and corporates, should materialize in the medium term, the negative impact on oil exporter countries, particularly on fiscal balances and the exchange rates, is more immediate and could be amplified by the energy export dependence for respective countries.

In a monetary policy context, the lower inflation observed in the euro area, for example, driven in part by the oil price decline, could de-anchor inflation expectations from the ECB’s target. Furthermore, in the US, the pressure on oil prices and subsequent pass-through to lower inflation levels could impact the economy in such a way as to delay the pace of normalisation of the Federal Reserve’s monetary policy. It should also be noted that (like in 1985) today’s low oil price is due to a combination of weak global demand and oversupply from oil-producer countries and hence, it is suggested, prices could stay stubbornly low for quite some time.

Figure 7. West Texas Intermediate (WTI) and Brent crude prices since 1984

%20and%20Brent%20crude%20prices%20since%201984.png) 3. Referendum on Brexit

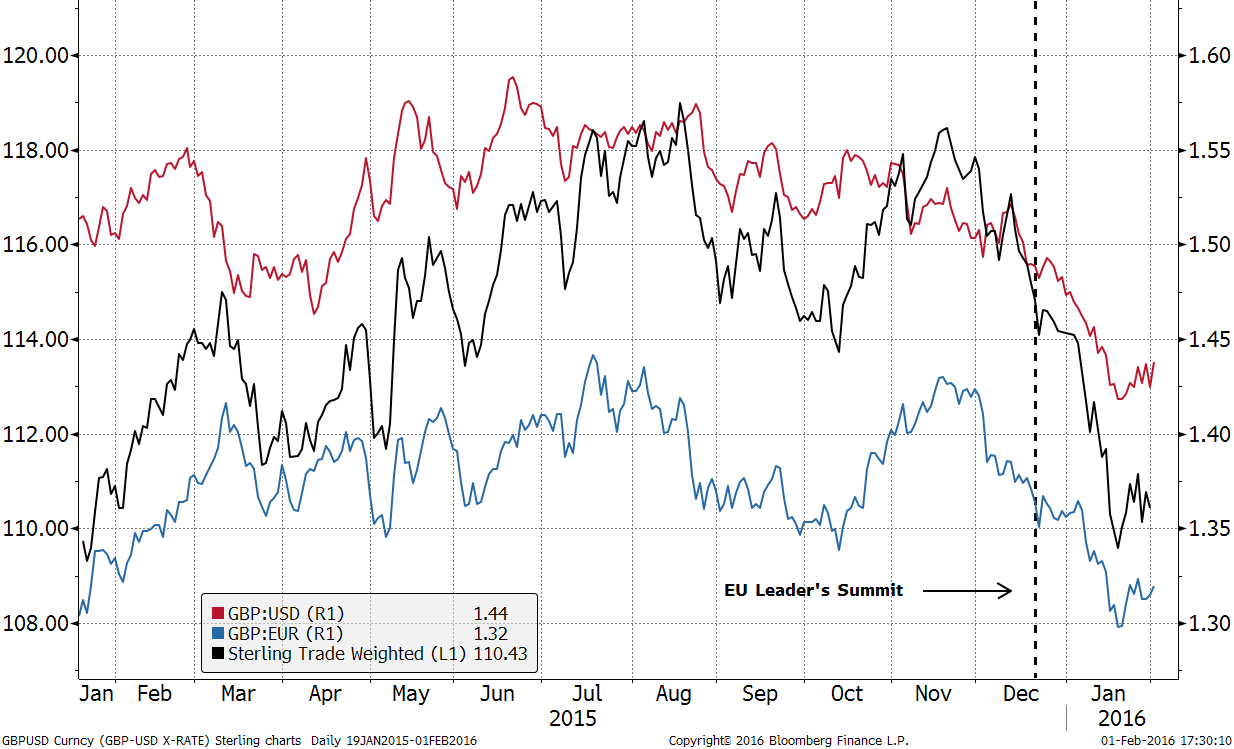

3. Referendum on Brexit

The UK has entered the final pre-election period for the referendum on Britain’s possible exit from the EU (Brexit), which will take place on 23 June 2016, the outcome of which is very uncertain at this stage. I will say a few more things on the importance of the British referendum for the rest of the EU tomorrow morning in my lecture on Europe’s political economy at the event hosted by the Singaporean-German Chamber of Industry and Commerce. Today, I will limit myself to only one comment. It seems that the weak pound is the only “certainty” across the spectrum of financial markets! Since the beginning of December, the British pound has lost over 7% and 5% of its value against the euro and the US dollar respectively (see Figure 8), with a portion of this decline in spot price being cited as a ‘Brexit’ premium by market participants.

Figure 8. British pound against US dollar and euro

However, in implying any direct causality between Brexit and the pound’s depreciation, we should remind ourselves that the recent pound depreciation has occurred in parallel with a reassessment of the likely rate path of the Bank of England, with expectations for the Bank of England to follow the Fed in raising interest rates, having decreased significantly over the same period with the market re-evaluating of the Bank of England’s potential interest rate path.

Thank you very much for your attention.

* Speech by Professor John (Iannis) Mourmouras, Deputy Governor of the Bank of Greece, at the “Asset and Risk Management Seminar for Public Sector Investors” organised by the Lee Kuan Yew School of Public Policy in association with OMFIF in Singapore, on 29 March 2016. Views expressed in this speech are personal views and do not necessarily reflect those of the Bank of Greece.