Commercial property indices: 2015 H2

30/05/2016 - Press Releases

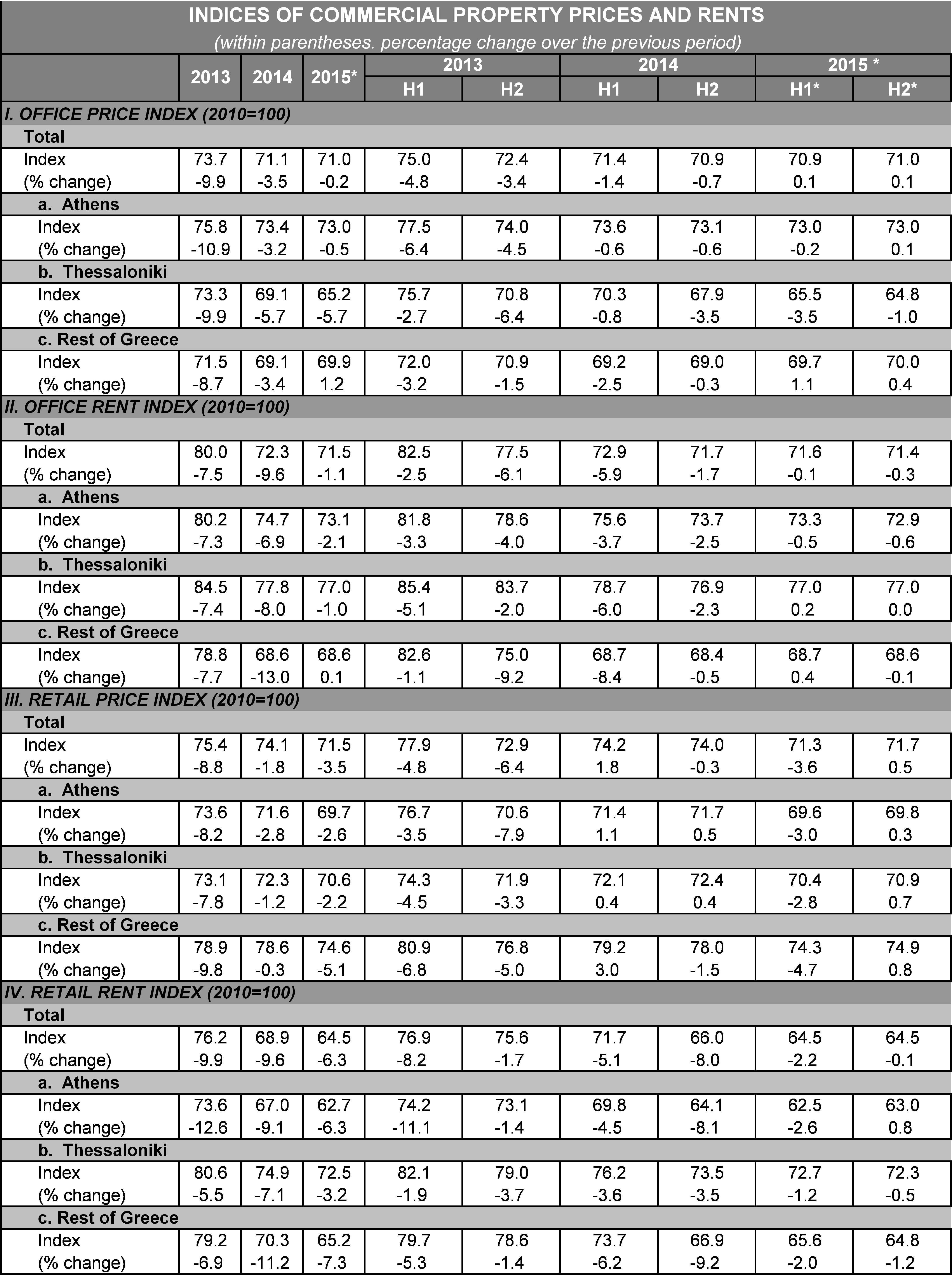

1. Office Indices

Office price index

According to provisional data in 2015, the annual rate of change in nominal prime office prices for the country as a whole was -0.2%, significantly weaker compared with 2014 (-3.5%) and 2013 (-9.9%). The corresponding average annual rates of decline were 0.5% for Athens and 5.7% for Thessaloniki, whereas an increase of 1.2% was recorded in the rest of Greece.

In the second half of 2015, nominal prime office prices for the country as a whole marginally increased by 0.1% compared with the first half of 2015 (provisional data). The respective rates of change recorded in the previous half-years were -0.7% for 2014 H2 and 0.1% for 2015 H1. Additionally, between the first and the second half of 2015, nominal prime office prices increased marginally in the greater Athens area (0.1%) and in the rest of Greece (0.4%), whereas a drop of 1.0% was recorded in Thessaloniki.

Office rent index

In 2015, office rents for the country as a whole decreased by 1.1% (provisional data) οn average in nominal terms. The corresponding average annual rates of decline are estimated at 2.1% in the greater Athens area and 1.0% in Thessaloniki, whereas a marginal increase of 0.1% was recorded in the rest of Greece.

In the second half of 2015, office rents for the country as a whole declined marginally by 0.3% compared with the first half of 2015 (provisional data), whereas in the previous half-years the respective rates were -1.7% for 2014 H2 and -0.1% for 2015 H1.

2. Retail indices

Retail price index

In 2015, the average annual rate of decline in prime retail prices for the country as a whole was 3.5% (provisional data) in nominal terms, which was accelerated compared with the corresponding rate in 2014 (-1.8%), but considerably slower compared with the rate in 2013 (-8.8%). The corresponding average annual rates of decline are estimated at 2.6% for the greater Athens area, 2.2% for Thessaloniki and 5.1% for the rest of Greece.

In the second half of 2015, prime retail prices for the country as a whole increased by 0.5% (provisional data) in nominal terms compared with the first half of 2015. The respective rates of change were -0.3% in 2014 H2 and -3.6% in 2015 H1. In the second half of 2015, nominal prime retail prices compared with the previous half-year increased by 0.3% in Athens, by 0.7% in Thessaloniki and by 0.8% in the rest of Greece.

Retail rent index

For 2015 as a whole, retail rents for the entire country declined on average by 6.3% (provisional data) in nominal terms. The respective rates of decline are estimated at 6.3% for the greater Athens area, 3.2% for Thessaloniki and 7.3% for the rest of Greece.

In the second half of 2015, retail rents for the country as a whole declined marginally by 0.1% (provisional data) compared with the first half of 2015. The rate of decline slowed down compared with the previous half-years (2014 H2: -8.0%, 2015 H1: -2.2%).

Detailed tables on retail and office prices and rents by geographical area are published in the “Bulletin of Conjunctural Indicators” (Tables ΙΙ.9, ΙΙ.10, ΙΙ.11 and ΙΙ.12, first published in Issue 162) and are also available on the Bank of Greece’s website, under “Real Estate Analysis”.

Source: Bank of Greece.

*Provisional data.

Notes:

1. For the purposes of monitoring and analysing the commercial property market, the Real Estate Market Analysis Section of the Bank of Greece compiles office and retail property indices, using data from credit institutions (Bank of Greece Executive Committee Act 23/26.07.2013) and Real Estate Investment Companies – REICs (Bank of Greece Executive Committee Act 9/10.01.2013) operating in Greece, as well as data from other sources, e.g. private real estate consultants, portfolio managers, real estate developers, real estate brokers and public sector entities. The data are collected on a biannual basis and include valuations, rents, transactions, investments and yields of commercial property and commercial property asset portfolios.

2. Indices are published on a biannual basis (base year: 2010). They concern office and retail uses and refer to price and rent levels of mainly prime investment property. It should be noted that price indices are valuation-based and are therefore expected to show some lag, especially in cases of negative changes. Furthermore, values tend to reflect sentiment and market expectations at the moment of the valuation, especially in periods of limited transactions.

3. The discrepancy between price and rent trends, recorded throughout 2014, can be explained by: i) the differences in the two samples (price indices are based on an A and upper B class investment property sample, whereas rent indices are based on a broader sample, from both the primary and secondary markets), ii) the fact that valuations – through yields – take into account sentiment and positive medium-term expectations and iii) the fact that a significant number of downward rent adjustments took place in 2014 (probably as a result of review processes that had started earlier, but were completed in 2014).